The rate has been reduced from 4.40% (biannual) to 2.92% (biannual). This change is effective for bonds issued from March 10, 2025, and applies to profit payments due after September 9, 2025.

Quick takeaway: Premium bond holders will receive lower biannual profit payouts going forward — the prize draw mechanics remain unchanged, but the guaranteed biannual profit is smaller than before.

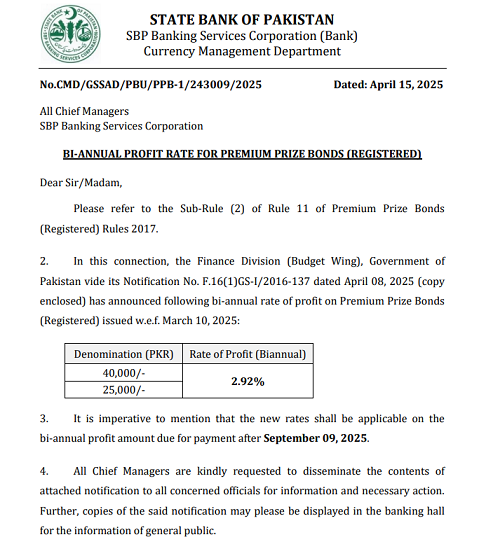

Official Rate Change & Effective Dates

The rate revision was announced through official channels. The essential facts are:

- Previous biannual profit rate: 4.40% (for both Rs. 40,000 and Rs. 25,000 premium bonds).

- New biannual profit rate: 2.92% (for both Rs. 40,000 and Rs. 25,000 premium bonds).

- Rates declared: effective for bonds issued w.e.f. March 10, 2025.

- Applicability on payments: The new rate will be applied to biannual profit amounts due for payment after September 9, 2025. In short — profit accruals and payouts scheduled after this date will reflect the new rate.

Source: State Bank of Pakistan / Finance Division notification. For the official circular, see the SBP announcement or contact your bank branch. (Public copies of circulars are also often posted on SBP’s website.)

Old vs New: Side-by-side Comparison

Below is a concise table that compares the previous and new biannual profit rates and highlights the arithmetic change for single-bond holdings.

| Denomination | Previous Biannual Rate | New Biannual Rate | Change (percentage points) |

|---|---|---|---|

| Rs. 40,000 (Premium) | 4.40% | 2.92% | -1.48 percentage points |

| Rs. 25,000 (Premium) | 4.40% | 2.92% | -1.48 percentage points |

Interpretation: A reduction of 1.48 percentage points on the biannual rate is substantial because premium prize bonds were promoted as a hybrid instrument — offering both the upside (prize draws) and a meaningful guaranteed biannual return. The reduction lowers the guaranteed part of their returns.

Why Was the Rate Reduced? — Economic & Policy Reasons

A policy decision like this typically stems from a mix of macroeconomic and fiscal considerations. Below we unpack the most relevant drivers.

1. Fiscal cost management

Premium prize bonds represent a government liability: payouts, including biannual profit, increase the state’s financing cost. Reducing the profit rate lowers recurring fiscal outflows associated with these instruments.

2. Alignment with market interest rates

Interest rates across the banking system and other government savings instruments influence what is considered “fair” compensation for low-risk instruments. When macro rates decline, governments often review guaranteed returns on public instruments to maintain policy coherence.

3. Monetary policy considerations

Central bank policy and liquidity management sometimes trigger secondary adjustments in government savings offerings. SBP and the Finance Division coordinate to ensure public savings instruments align with broader monetary and fiscal objectives.

4. Incentivizing efficient allocation of savings

Lower guaranteed returns on premium bonds may encourage retail investors to allocate some savings into higher-yielding or more productive instruments (mutual funds, government securities, private sector deposits, or long-term savings schemes), potentially supporting capital formation and investment.

Note: The government still maintains prize draws unchanged, which preserves some speculative upside for holders.

Impact on Investors — A Detailed Analysis

This section breaks down how the rate change affects different investor groups: single-bond holders, moderate portfolios, and large retail holders (savers and small businesses).

1. Single-bond holders

For an individual holding a single premium bond, the numerical impact is modest but visible:

| Denomination | Old Biannual Profit (4.40%) | New Biannual Profit (2.92%) | Absolute reduction (per biannual) | Reduction per year (annualized) |

|---|---|---|---|---|

| Rs. 40,000 | Rs. 1,760 | Rs. 1,168 | Rs. 592 | Rs. 1,184 |

| Rs. 25,000 | Rs. 1,100 | Rs. 730 | Rs. 370 | Rs. 740 |

In plain words, each Rs. 40,000 bond will yield Rs. 1,184 less per year in guaranteed profit than before; each Rs. 25,000 bond will yield Rs. 740 less per year. For low-income savers who rely on regular profit, this reduction can be meaningful.

2. Moderate portfolios (10–100 bonds)

Investors holding multiple bonds will see proportional declines in guaranteed returns. A moderate portfolio of 10 x Rs. 40,000 (Rs. 400,000 total nominal holding) will lose Rs. 11,840 per year in guaranteed income—amounts that matter for household budgets and cash-flow planning.

3. Large retail holders & institutional investors

Larger holders or trusts using premium bonds as a low-risk income source will need to reassess cash-flow models. Reduced guaranteed returns may prompt partial reallocation of funds to higher-yielding government or private instruments.

4. Prize-draw dependent investors

The prize-draw aspect remains unchanged. For many investors, particularly those who buy prize bonds for the chance at large prizes rather than the guaranteed profit, the portfolio calculus may not change materially — they still benefit from occasional large wins. However, for those who relied on the combined guarantee + prize structure as a more predictable income stream, the reduced guarantee lowers the expected value of holding a premium bond.

Worked Examples & Precise Arithmetic (so there’s no confusion)

Below are step-by-step calculations for different holdings. We present exact arithmetic so readers can replicate the figures or plug in their own numbers.

Example 1 — One Rs. 40,000 premium bond

Old biannual profit: 4.40% of 40,000 = 0.044 × 40,000 = Rs. 1,760 (every six months)

Annual equivalent: 1,760 × 2 = Rs. 3,520 per year.

New biannual profit: 2.92% of 40,000 = 0.0292 × 40,000 = Rs. 1,168 (every six months)

Annual equivalent: 1,168 × 2 = Rs. 2,336 per year.

Annual drop in guaranteed profit: 3,520 − 2,336 = Rs. 1,184.

Example 2 — Five Rs. 25,000 premium bonds (total Rs. 125,000)

Old biannual profit (per bond): 4.40% of 25,000 = Rs. 1,100 (six-month payout)

Total old annual profit: (1,100 × 2) × 5 = Rs. 11,000 per year.

New biannual profit (per bond): 2.92% of 25,000 = Rs. 730 (six-month payout)

Total new annual profit: (730 × 2) × 5 = Rs. 7,300 per year.

Annual reduction: 11,000 − 7,300 = Rs. 3,700 lost per year in guaranteed returns.

Example 3 — Portfolio of 100 x Rs. 40,000 bonds (nominal Rs. 4,000,000)

Old annual guaranteed profit: Rs. 3,520 × 100 = Rs. 352,000 per year.

New annual guaranteed profit: Rs. 2,336 × 100 = Rs. 233,600 per year.

Annual reduction: Rs. 118,400.

These calculations are exact and simple multiplication of the bond nominal value by the stated percentages. If you have multiple holdings or mixed denominations, sum the expected old and new totals to compute your impact.

Alternative Investment Options — Where Might Savers Shift?

When guaranteed returns fall on a safe instrument, rational investors look for alternatives that match their risk appetite and liquidity needs. Below we list viable options in Pakistan, together with general pros and cons.

1. National Savings Schemes

Instruments like Behbood Savings Certificates, Regular Income Certificates, and other National Savings products often offer competitive fixed rates — especially for long tenures or targeted segments (pensioners, widows, senior citizens). These are government-backed and low-risk.

Official resource: National Savings Pakistan.

2. Government Marketable Securities

Treasury bills and Pakistan Investment Bonds (PIBs) are market instruments. They are liquid (T-bills especially), and yields are determined by auction — often reflecting prevailing market interest rates.

3. Bank Deposits & Fixed-Term Accounts

Term deposits and savings accounts may offer competitive rates, and many banks offer special term deposit products with attractive yields for specific tenures. These are covered by commercial banks and have differing liquidity and penalty structures.

4. Mutual Funds & Pension Funds

For investors willing to accept moderate volatility for potentially higher long-term returns, open-end mutual funds (income funds, balanced funds) provide diversification and professional management. Check fund performance, expense ratios, and track records.

5. Corporate Fixed Income

Corporate debt instruments (certificates, bonds) sometimes provide yields above government instruments, but they carry credit risk. Choose issuers carefully and view credit ratings.

Use our Investment Strategies page for a direct comparison of options and a simple decision framework.

Practical Strategies for Current Premium Bond Holders

If you already hold premium prize bonds, here are pragmatic steps you can take right now. These are structured to respect different investor profiles (conservative, balanced, and growth-oriented).

Conservative: Keep core holdings, adjust expectations

- Retain a portion of your premium bonds if they form part of a security-first portfolio.

- Recalculate cash-flow: update expected biannual profit figures and note the timing of changes after Sept 9, 2025.

- If profit payouts are an important monthly/quarterly income, consider reallocating a small portion into short-term government bills or bank term deposits to partially offset the reduction.

Balanced: Partial diversification

- Redeem a fraction of premium bonds to free up capital.

- Place proceeds into a mix of National Savings for stability and an income mutual fund for a chance of higher returns.

- Use staggered maturities or laddered deposits to manage reinvestment risk.

Growth-oriented: Active reallocation

- If you have a higher risk tolerance, consider redirecting capital into diversified equity mutual funds or long-term government bonds (PIBs) when yields are attractive.

- Maintain a small allocation to premium bonds purely for prize-draw exposure — keep the “lottery plus interest” flavor of the instrument without over-relying on its reduced guaranteed yield.

Remember: any move should respect your liquidity needs, tax situation, and financial goals. If unsure, consult a financial advisor.

Calculate your premium prize bond profit

Frequently Asked Questions (FAQs)

Q1: What exactly changed, and when will it affect payouts?

Answer:

The biannual profit rate on premium prize bonds (both Rs. 25,000 and Rs. 40,000) was revised from 4.40% to 2.92%. The rates apply to bonds issued w.e.f. March 10, 2025, and specifically affect profit payments that fall due after September 9, 2025. Payouts scheduled before this date should remain at the previously applicable rate if they correspond to earlier accrual periods.

Q2: Will the prize amounts in draws change?

Answer:

No. The prize draw structure — first prize, second prize, third prize amounts and the draw schedule — is separate from the biannual profit rate. The rate change impacts the guaranteed biannual profit only, not the prize money awarded in draws.

Q3: Are older bonds affected?

Answer:

Bonds issued before March 10, 2025 remain in the system, but the new rate applies to profit payments due after September 9, 2025. Practically, any profit installment that becomes payable after that date will reflect the changed rate per the official circular details.

Q4: Should I redeem my premium prize bonds now?

Answer:

There is no universal answer. Consider your liquidity needs and whether the prize-draw upside still matters to you. If you hold bonds for guaranteed income, the rate reduction may motivate partial redemption and reinvestment in other instruments. For pure prize-chasing investors, the decision may be different.

Q5: Where can I find the official notification?

Answer:

The rate change was communicated via official channels. You can check SBP’s website and the Finance Division circular for the formal notification. (SBP publishes circulars on its site periodically.)

Conclusion & Next Steps

The shift from 4.40% to 2.92% on the biannual profit rate for premium prize bonds is a notable policy move with real implications for savers across Pakistan. While the prize draws continue to provide gambler-style upside, the reliable, guaranteed portion of returns has shrunk.

Practical next steps for readers:

- Update your personal portfolio spreadsheet to reflect new profit figures for payouts after September 9, 2025.

- Decide whether to partially redeem or reallocate funds based on your income needs and risk appetite.

- Compare alternatives (National Savings, bank deposits, government securities, and mutual funds).

- Monitor official releases from SBP and Finance Division for any further changes.

Stay informed with our live coverage and tools:

Resources & References

Official references and useful external sources:

- State Bank of Pakistan (SBP) — official circulars and notifications. Visit: https://www.sbp.org.pk/

- National Savings Pakistan — official site for government savings instruments and current rates: https://savings.gov.pk/

- PrizeBond.Shalkot.com internal pages:

Note: We encourage readers to consult official circulars and their bank branches for specific account- or bond-related queries. This article is intended for general information and does not constitute financial advice.

Disclaimer

The information provided on this page is for educational and informational purposes only. While we strive to keep content accurate and up-to-date, official policies and rates are determined by the Government of Pakistan and the State Bank of Pakistan. For exact legal or financial guidance, please consult a licensed advisor or the official government notifications.