Best Investment Options in Pakistan for 2025—Where to Put Your PKR

In this long guide, we compare safe, medium, and high-return investments for Pakistan in 2025—Naya Pakistan Certificates (NPC), bank FDs, prize bonds, mutual funds, stocks, gold, and practical portfolios you can implement today.

Snapshot — What matters in Oct 2025

- SBP policy rate: 11.00% (Oct 2025). This guides bank deposit yields and short-term instrument rates.

- Inflation (Urban CPI): ~5.5% YoY in September 2025 — important for real returns.

- Naya Pakistan Certificate (NPC) headline rates (Oct 2025): PKR tranches show attractive annualized returns (3M/6M/12M/3Y/5Y). Always confirm with your bank for current weightages.

- Stock market: KSE-100 around ~163,000–165,000 in mid-Oct 2025; markets are volatile but show pockets of opportunity.

- Macro update: Pakistan reached a staff-level IMF deal in October 2025, which supports economic stability and helps confidence in bond & currency markets.

Why this guide—a practical investor framework

This article helps you decide which instruments best match your goals and risk tolerance in 2025. We separate options into safe/income (low risk), balanced, and growth/aggressive.

Table of contents

- Safe / Income Options—NPC, Bank FDs, High-yield Savings

- Low-Volatility Alternatives—Prize Bonds & Government Papers

- Balanced Growth—Mutual funds & asset allocation

- Growth/Aggressive—Stocks & private equity

- Hedge assets—gold & foreign currencies

- Sample portfolios by risk profile

- How to choose & avoid common mistakes

- Infographic, PDF download & next steps

1) Safe / Income (Low risk)—who it’s for and why

Safe options are for capital preservation and predictable returns. If you need money within 1–5 years, prioritize these.

Naya Pakistan Certificates (NPC)

NPCs are government-backed securities available in PKR and foreign currency tranches with multiple tenors (3M, 6M, 12M, 3Y, 5Y). For October 2025, PKR annualized rates were competitive (see SBP/Bank weightages)—they remain a top pick for conservative investors seeking yields above inflation. Always confirm the bank’s announced weightages before investing.

Why NPC may be right for you

- Government-backed principal safety

- Attractive fixed/expected returns (PKR tranche often > inflation)

- Multiple tenors to match liquidity needs

Practical steps to buy NPC

- Compare NPC weightages announced by multiple banks—most banks publish an “expected PSR/weightage” PDF monthly.

- Complete bank KYC; some banks allow online subscription; others require a visit.

- Choose a tenor matching your goal: short-term (3–12 months) if you need liquidity; 3–5 years for a higher yield if you can lock money.

Bank Fixed Deposits (Term Deposits / FDs)

Bank FDs are convenient and widely available. With the SBP policy rate near 11% in Oct 2025, short/medium FDs can be competitive. Compare early withdrawal penalties, compounding frequency, and effective annual yield.

2) Low-volatility alternatives

Prize Bonds

Prize bonds are non-interest, lottery-style instruments. They provide a chance at large prizes but no guaranteed interest. Keep prize bonds as a small allocation (entertainment/speculation) and not as your core capital preservation vehicle. Use them when you want liquidity and upside without locking funds. See our prize bond pages for draw calendars and result-checking tools.

Government papers & T-bills

Short-term Treasury Bills (MTBs) and Pakistan Investment Bonds (PIBs) are useful for institutions and conservative investors. Yields track SBP rates and are appropriate for short-term parking of funds.

3) Balanced—moderate risk & growth

Mutual Funds (AMC-managed)

Mutual funds offer pooled exposure to stocks, bonds, or mixed assets. For investors who want diversification without stock picking, consider:

- Income/money market funds—for near-cash returns

- Balanced/asset allocation funds—automatically rebalance between equity and debt

- Equity funds—for higher long-term returns (5+ years horizon)

Use monthly systematic contributions (SIP-style) to smooth market volatility. Check AMCs’ track record (3–5 year returns, manager tenure, fees).

4) Growth / Aggressive

Stock market / Individual equities (PSX)

Stocks deliver the highest long-term returns but are volatile. As of mid-Oct 2025, the KSE-100 traded around ~163,000–165,000 and showed both corrections and rallies—opportunities exist, but select stocks using fundamentals (earnings, cash flow, industry tailwinds). Always apply position sizing and stop-loss discipline.

Private equity & small business

For accredited or experienced investors, private equity or starting a small business can produce outsized returns—but these require time and active management. Allocate only what you can afford to illiquidity and risk.

5) Hedge assets

Gold

Gold remains a useful hedge against currency volatility and inflation. Consider local price spreads, making charges (if buying jewelry), and storage security. For exposure without physical custody, look at bank gold accounts or sovereign gold bonds if available.

Foreign currency exposure

Holding some USD or other strong currencies hedges PKR depreciation risk. Use authorized bank forex products or foreign-currency NPC tranches—check bank rules for remittance limits and tax treatment.

6) Sample portfolios (suggested allocations)

Conservative (safety-first)

- NPC & Bank FDs: 60%

- Money-market/income funds: 20%

- Prize Bonds: 5%

- Gold & FX hedge: 10%

- Stocks (high-quality): 5%

Balanced (growth + income)

- NPC/FDs: 30%

- Mutual funds (balanced): 25%

- Stocks: 20%

- Gold & FX: 10%

- Prize Bonds & cash: 15%

Aggressive (growth-focused)

- Stocks & equity funds: 50%

- Mutual equity funds: 20%

- Small business / private equity: 15%

- Gold & FX: 10%

- Liquid cash/NPC short-term: 5%

7) How to choose—a step-by-step checklist

- Define horizon: when will you need the money?

- Determine risk tolerance: can you stomach 20–40% swings?

- Match instruments to horizon (liquid for <1 year, diversified for 3–7, equity for 7+).

- Compare real returns (nominal minus expected inflation).

- Factor in taxes, fees, and exit costs.

8) Common mistakes & how to avoid them

- Chasing headlines & hot tips—invest with a plan, not FOMO.

- Ignoring diversification—don’t put everything in one stock or instrument.

- Over-allocating to speculative prizes (prize bonds) when you need stability.

- Not checking NPC/FD effective yields after taxes and bank charges.

9) Tactical ideas for 2025 (based on current macro)

With the SBP policy rate at 11% and inflation near 5.5% (Sept 2025), short/medium-term NPC and bank FDs offer positive real yields; stocks may benefit from improved macro confidence after the IMF staff-level deal in Oct 2025, but volatility remains. Balance liquidity and yield—keep an emergency fund liquid while locking a portion in NPC or FDs for yield.

10) Practical platform & execution tips

- Open accounts in at least two banks for rate shopping

- Use AMC portals for mutual funds; start small SIPs monthly

- Keep documentary records for tax filing and KYC

- Use trusted dealers if buying physical gold

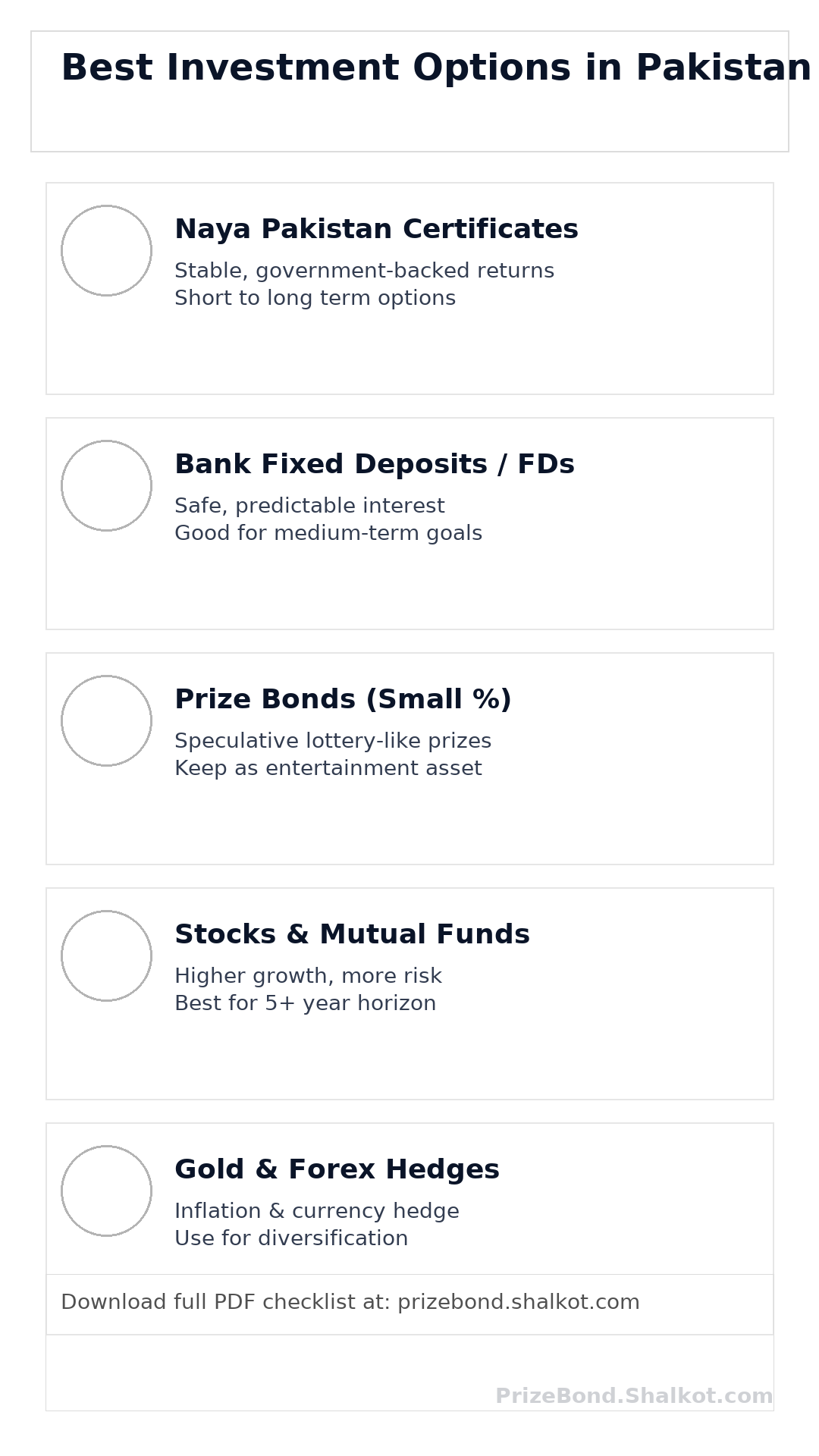

11) Infographic & downloadable PDF

Quick infographic — Best Investment Options (2025)

Preview (downloadable):

Download Printable PDF — Investment Checklist

Tip: Upload these files to your WordPress media library and update the links above to use your CDN/https URLs. The PNG is optimized for social sharing (1080×1920), and the PDF is printable for leaflets or newsletter attachments.

12) YouTube Short—SEO trick

Create a 30–45 second YouTube Short that highlights one “Top Investment Pick for 2025” (e.g., NPC vs FD). Embed it in the article to increase time-on-page and cross-platform traffic.

13) SEO & sharing checklist (publish-ready)

- Title (CTR tested): “Best Investment Options in Pakistan 2025—NPC, Stocks, Gold & How to Build Your Portfolio”

- Meta description: Use the copy at the top; keep under 155 characters for SERP.

- Schema: Keep JSON-LD up-to-date with dateModified on every update.

- AMP: Publish an AMP version and link through for mobile speed.

- Sitemap: Submit the sitemap weekly if you publish multiple posts—GSC > Sitemaps.

14) Comments & community engagement

What do readers say?

“Which one are you using today? Reply below — I will publish a readers’ portfolio roundup every month.”

15) Final recommendations—one-month, 6-month & 12-month plan

1 month: Open accounts, set aside emergency fund (1 month), buy short-term NPC or liquid FD for target amount.

6 months: Build a 3-month emergency fund, start SIPs in a balanced mutual fund, and allocate a small percentage to prize bonds if you like the upside.

12 months: Rebalance portfolio to target allocation (conservative, balanced, or aggressive). Evaluate performance and adjust for life changes.